Article

Future Outlook of Autonomous Delivery Vehicles

Mobility

Introduction

In the last few months, the COVID-19 pandemic has caused global supply chain disruptions across various sectors such as healthcare, industrial manufacturing, construction, and retail. The concern is not only the non-availability of goods/material but also about the transportation and delivery of the goods/material available. The primary problem is also the non-availability of human labor for delivery. In this unprecedented situation, there is a growing opportunity for autonomous delivery vehicles (hereinafter, ADV) to address the delivery demand and reduce virus spread. Further, due to social distancing norms, the rise of e-commerce continues, and companies around the globe are increasingly getting sensitive to changing consumer lifestyles. For retail, restaurant & food chains, and e-commerce companies, autonomous delivery is one of the most important emerging technology today. According to Sterling Hawkins, co-founder of CART, the Center for Advancing Retail & Technology, a platform that connects brands and retailers with emerging technology solutions, automated delivery could be transformational for the industry, which can help reduce delivery costs by 80% to 90% compared to a human doing it, depending on the vehicle and the platform. In this scenario, ADVs are in high demand considering they can safely perform the last-mile delivery operation. Apart from the COVID-19 pandemic, the global population is expected to reach 8.5 billion by 2030, with 60% of people living in cities, accounting for 70% of global emissions. This increase in urban populations will cause exponential increases in congestion with some contribution from passenger cars but a much more disproportionate contribution by the delivery vehicles. ADV can be a cost-effective answer to this, along with answering some other issues, such as increasing global population and environmental concerns.Growing market of Autonomous Delivery Vehicles

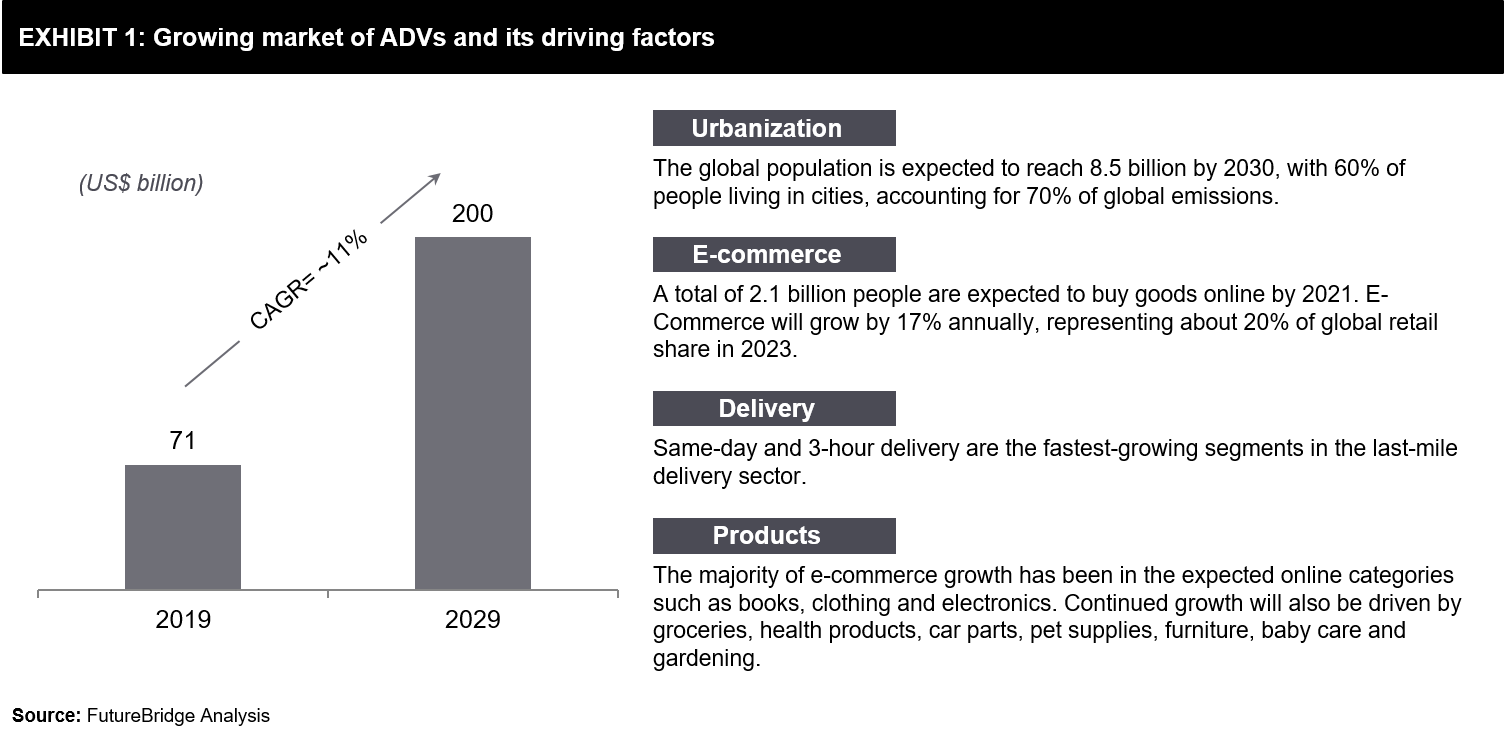

The market demand for ADVs is poised for significant growth in the next 7–9 years. The market is expected to grow at an 11% CAGR from 2019 to reach $200 billion in 2029. Following are the various factors that are driving its demand:

- Urbanization: As per the WEF report, the global population is expected to reach 8.5 billion by 2030, with 60% of people living in cities, accounting for 70% of global emissions.

- E-Commerce customers: A total of 2.1 billion people are expected to buy goods online by 2021. E-Commerce will grow by 17% annually, representing about 20% of the global retail share in 2023. This will cause significant increases in the number of parcels being shipped globally, with massive increases in high-growth regions like China.

- Products: The majority of E-commerce growth has been in the expected online categories, such as books, clothing, and electronics. This will continue to grow in the coming years. However, the overall increase in the sector will be driven by new categories, including groceries, health products, car parts, pet supplies, furniture, baby care, and gardening.

- Expected delivery time: Same-day and 3-hour delivery are the fastest-growing segments in the last-mile delivery sector. While standard delivery will continue to be the largest delivery segment, the demand for speed from consumers will result in more online orders shipped individually, drive significant increases in the overall number of deliveries.

- Technological developments: Developments in last-mile technology, including drones, droids, and automated fulfillment centers, will increase both the speed and processing capacity for logistic providers. Alibaba alone is investing an estimated $15 billion in logistics automation and driverless technology over the next five years.

Types of ADVs and their current challenges

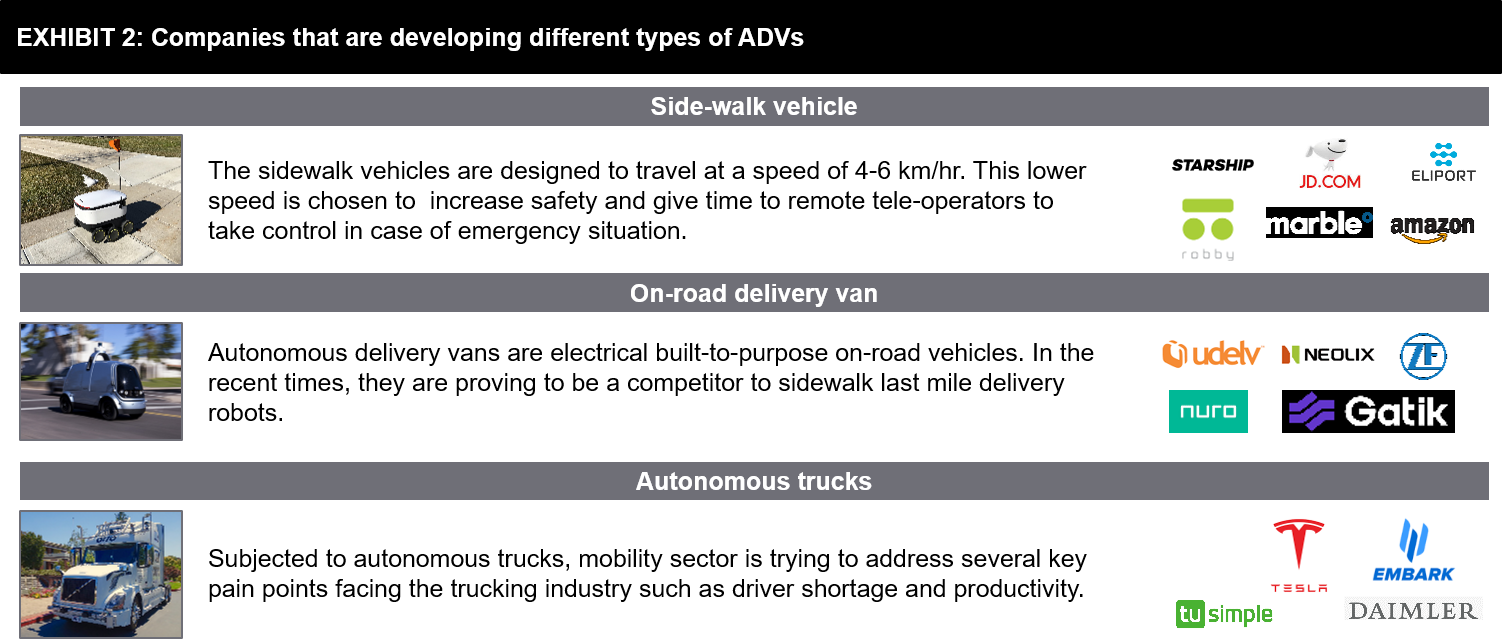

Many companies are developing different types of ADVs that can be categorized into side-walk vehicles, on-road delivery vans, and autonomous trucks. These companies are focusing on last-mile delivery as it is the most expensive part of the delivery chain that represents more than 50% of the overall cost. In recent years, companies are utilizing autonomous mobile robots, and autonomous vehicle technology to automate this step. The following exhibit illustrates some of the companies that are developing different types of ADVs: Side-walk vehicles

The sidewalk vehicles are designed to travel at a speed of 4-6 km/hr. This lower speed is chosen to increase safety and give time to remote teleoperators to take control in case of an emergency. Based on the individual use, these vehicles can also be categorized as a personal device (vs. a vehicle), thus easing the legislative challenges.

This vehicle type has to be developed based on the number of motor-controlled wheels, payload size, compartment design, battery size, HD cameras. Also, IMUs, GPS, and ultrasound sensors are important for near-field sensing.

Currently, various sidewalk vehicle developers have to make an important choice for the vision system. There are three ways to have a vision system, either only lidar-based, only stereo-camera, or hybrid. Most of the companies prefer having lidar as it gives 3600 ranging information with spatial resolution and a point cloud to have good signal processing. However, on the downside, lidars are expensive and can have a near-field blindspot. The other approach of having a stereo camera as the navigation sensor requires the development of accurate algorithms, which is considered difficult by various companies.

Based on this current navigation challenge coupled with regulatory challenges, these sidewalk vehicles are yet to be seen running fully autonomous. They are currently deployed in closed environments such as university campuses that have little sidewalk traffic, and the sidewalks are well-structured. Also, these vehicles are restricted from operating in daylight and perception-free conditions. Therefore, various companies and regulatory authorities have eyes on the improvements of navigation technology. Companies are also focusing on having these vehicles operate in more complex and varied environments with minimal intervention.

Furthermore, the future of side-walk vehicles will depend on having constant technology improvements, which can be made possible by having continuous capital investments.

Autonomous Delivery Trucks and Vans

Autonomous delivery vans are electrical built-to-purpose on-road vehicles. In recent times, they are proving to be a competitor to sidewalk last-mile delivery robots. Their sensor system and algorithms are similar to autonomous cars, although the following considerations are made to ease the technical burden:

On-road delivery pods travel slowly; therefore, the perception of technology is not long-ranged. This gives the autonomous vehicle more thinking and reaction time.

These on-road delivery pods are deployed in limited known neighborhood areas, thus allowing more detailed HD maps to be developed to aid autonomous navigation.

Subjected to autonomous trucks, the mobility sector is trying to address several key pain points facing the trucking industry, such as driver shortage and productivity. Concerning driver shortage, it is estimated to reach 150k persons by 2028 in the US alone. Increasing productivity is difficult as the legislation limits drive time per driver per day, thus decreasing asset up time in favor of increasing safety.

Since late 2016, various start-ups have raised more than $430M to enable autonomous trucks. Major automotive companies such as Daimler have announced significant investment plans for the next five years. Companies are also in the semi-commercial prototyping phase, wherein the focus is on the level of autonomy and platooning.

Looking at the autonomy level, companies have different approaches based on the deployed sensing system. Some companies are using camera-based algorithms for navigation and have human teleoperators in case the truck is in complex environments. Some companies have a mixed approach wherein. The camera scans the long-distance, and lidars only focus on objects of interest within the few 100-meter radii. This mixed approach is made to overcome the challenge of using lidar for very long-range detection that results in high power consumption and signal-to-noise ratio.

In all, current deployed autonomous trucks are low in numbers, with companies having a fleet of 30 to 50. In the coming years, it is expected this fleet number will expand due to COVID-19. However, on the technology improvement side, it is expected these autonomous trucks will be in the trial phase to focus on collecting data to improve the learning further.

Side-walk vehicles

The sidewalk vehicles are designed to travel at a speed of 4-6 km/hr. This lower speed is chosen to increase safety and give time to remote teleoperators to take control in case of an emergency. Based on the individual use, these vehicles can also be categorized as a personal device (vs. a vehicle), thus easing the legislative challenges.

This vehicle type has to be developed based on the number of motor-controlled wheels, payload size, compartment design, battery size, HD cameras. Also, IMUs, GPS, and ultrasound sensors are important for near-field sensing.

Currently, various sidewalk vehicle developers have to make an important choice for the vision system. There are three ways to have a vision system, either only lidar-based, only stereo-camera, or hybrid. Most of the companies prefer having lidar as it gives 3600 ranging information with spatial resolution and a point cloud to have good signal processing. However, on the downside, lidars are expensive and can have a near-field blindspot. The other approach of having a stereo camera as the navigation sensor requires the development of accurate algorithms, which is considered difficult by various companies.

Based on this current navigation challenge coupled with regulatory challenges, these sidewalk vehicles are yet to be seen running fully autonomous. They are currently deployed in closed environments such as university campuses that have little sidewalk traffic, and the sidewalks are well-structured. Also, these vehicles are restricted from operating in daylight and perception-free conditions. Therefore, various companies and regulatory authorities have eyes on the improvements of navigation technology. Companies are also focusing on having these vehicles operate in more complex and varied environments with minimal intervention.

Furthermore, the future of side-walk vehicles will depend on having constant technology improvements, which can be made possible by having continuous capital investments.

Autonomous Delivery Trucks and Vans

Autonomous delivery vans are electrical built-to-purpose on-road vehicles. In recent times, they are proving to be a competitor to sidewalk last-mile delivery robots. Their sensor system and algorithms are similar to autonomous cars, although the following considerations are made to ease the technical burden:

On-road delivery pods travel slowly; therefore, the perception of technology is not long-ranged. This gives the autonomous vehicle more thinking and reaction time.

These on-road delivery pods are deployed in limited known neighborhood areas, thus allowing more detailed HD maps to be developed to aid autonomous navigation.

Subjected to autonomous trucks, the mobility sector is trying to address several key pain points facing the trucking industry, such as driver shortage and productivity. Concerning driver shortage, it is estimated to reach 150k persons by 2028 in the US alone. Increasing productivity is difficult as the legislation limits drive time per driver per day, thus decreasing asset up time in favor of increasing safety.

Since late 2016, various start-ups have raised more than $430M to enable autonomous trucks. Major automotive companies such as Daimler have announced significant investment plans for the next five years. Companies are also in the semi-commercial prototyping phase, wherein the focus is on the level of autonomy and platooning.

Looking at the autonomy level, companies have different approaches based on the deployed sensing system. Some companies are using camera-based algorithms for navigation and have human teleoperators in case the truck is in complex environments. Some companies have a mixed approach wherein. The camera scans the long-distance, and lidars only focus on objects of interest within the few 100-meter radii. This mixed approach is made to overcome the challenge of using lidar for very long-range detection that results in high power consumption and signal-to-noise ratio.

In all, current deployed autonomous trucks are low in numbers, with companies having a fleet of 30 to 50. In the coming years, it is expected this fleet number will expand due to COVID-19. However, on the technology improvement side, it is expected these autonomous trucks will be in the trial phase to focus on collecting data to improve the learning further.