Forging Change: Reducing Emissions in the Steel Sector

Executive Summary

With the steel industry currently contributing 8-10% to global emissions, can we afford to delay its decarbonization? It’s not just about hitting targets; it’s about our planet’s future. Decarbonizing steel isn’t an option; it’s a necessity if we’re serious about combating climate change head-on. The challenge is to find suitable replacements to traditional processes that use coal both as a fuel for heating and as a reducing agent. The incorporation of hydrogen and biomass as a reducing agent has delivered promising outcomes, marking a substantial 20-40% reduction in emissions. Green hydrogen-based DRI technology can attain reductions of 97% but at very high costs. The potential solutions could be in technologies like renewable energy-powered electrolysis and combinations of carbon capture.

Introduction

With an annual global production nearing 2 billion metric tons per year, steel ranks third globally among man-made bulk materials, after cement and timber. Steel demand is expected to rise 30% by 2050, driven by the increasing need for clean energy infrastructure. However, traditional steel industry practices are highly carbon and energy-intensive, and the steel industry emitted approximately 91 tons of CO2 in 2022 for each ton of produce accounting for 8 -10% of global emissions. The steel industry’s emissions are “hard to abate” in nature given the extended asset lifetimes and high replacement costs to meet net-zero goals and align with the Paris Agreement. Achieving the Paris Agreement’s goal of limiting global warming to 1.5°C requires a 90% reduction in direct emissions and carbon intensity from the steel sector by 2050.

Innovative decarbonization strategies are thus crucial for the sector to enable a swift and comprehensive transformation toward carbon neutrality.

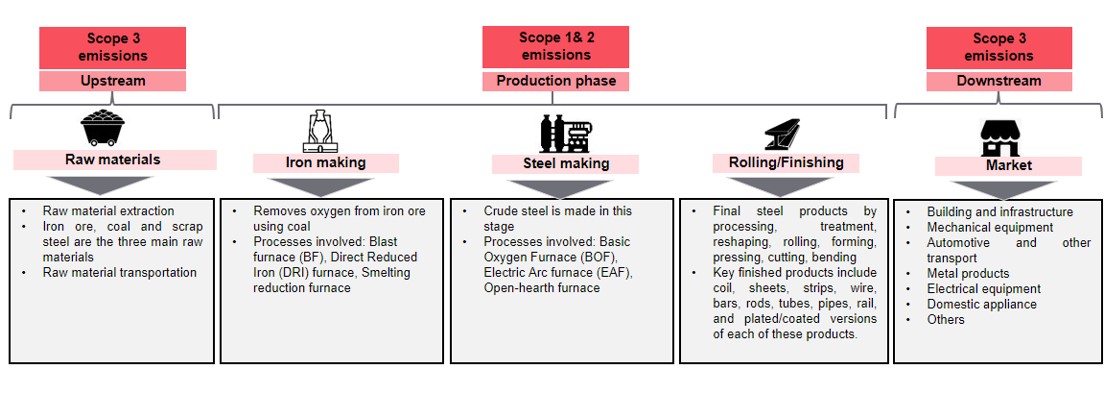

Emissions across the steel industry value chain

Operations tied to iron and steel production have emissions majorly fall under the categories of:

- Scope-1 which are direct emissions

- Scope-2 emissions resulting from the usage of electricity

- Scope-3 emissions, stemming from upstream activities like iron and coal mining and downstream activities such as selling finished steel products, though difficult to address, have a very limited share in this sector.

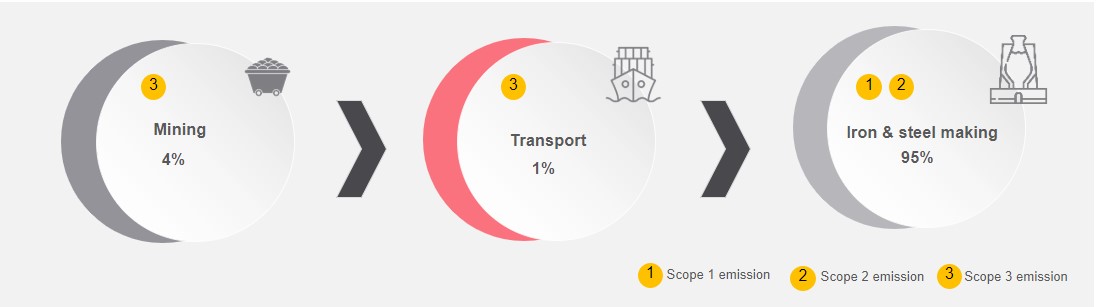

Iron and steel production alone contributes to approximately 95% of total emissions across the steel making value chain, primarily driven by the extensive use of the Blast Furnace-Basic Oxygen Furnace (BF-BOF) process.

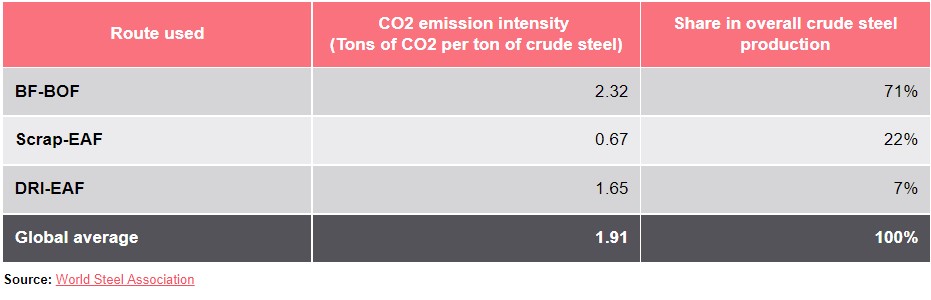

Steel production routes and their environmental impact

71% of global primary steel production is through the conventional blast furnace-basic oxygen furnace (BF-BOF) process, utilizing coal as both energy source and reducing agent. This method, widely employed in China, Japan, Germany is the most emissions-intensive and accounts for the bulk of emissions. The Direct Reduction (DR) method has a share of 7 and mainly relies on natural gas and is thus prevalent in gas-producing countries like Iran, Russia, and Saudi Arabia. The secondary (recycled) steelmaking process using an Electric Arc Furnace (EAF) is the least emissions-intensive of the conventional routes and constitutes the remaining 22% of global steel production.

Decarbonization pathways for iron and steel

As pressure for decarbonization mounts on the sector, there is a pressing need to explore and adopt innovative approaches that can significantly lower emissions while still ensuring production efficiency.

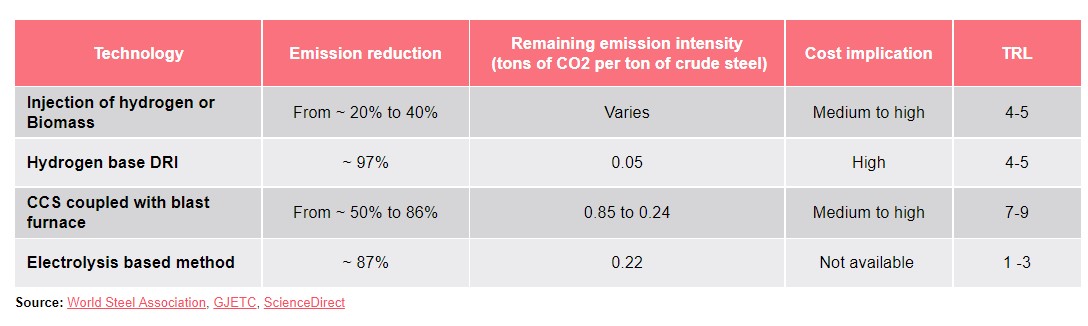

The key decarbonization technologies being considered by leading players in the sector for achieving near-zero emissions in steel production include:

- Injection of hydrogen or biomass involves the introduction of biomass or hydrogen into the blast furnaces or using biomass in a DRI furnace. This approach aims to reduce the reliance on fossil fuels. Biomass and hydrogen can significantly reduce emissions, but the overall potential is limited by the sustainably available biomass and the carbon intensity of hydrogen production.

- The hydrogen-based Direct Reduction of Iron (DRI) process focuses on the use of hydrogen as both an energy source and a reducing agent in steel making process. If green hydrogen is used – which is completely generated from renewable sources, it can achieve zero-emission goals. It has a high CO2 reduction potential but comes with implications of a higher cost.

- Carbon Capture Storage (CCS) coupled with blast furnace focuses on capturing CO2 emissions at the source during iron and steel production, and either storing it underground or utilizing it for purposes such as enhanced oil recovery (EOR) or production of chemicals or fuels.

- Electrolysis-based method whereby iron ore is dissolved in a solvent at 1600oC and electric current is passed through it. Negatively charged oxygen ions migrate towards the positively charged anode and get released. Positively charged iron ore migrate to the negatively charged cathode where they are reduced to molten iron. If the electricity is carbon-free, then the iron thus produced can be claimed to be without emissions. However, this technology has a lower technology readiness level (TRL) and would need further time for maturation and commercialization.

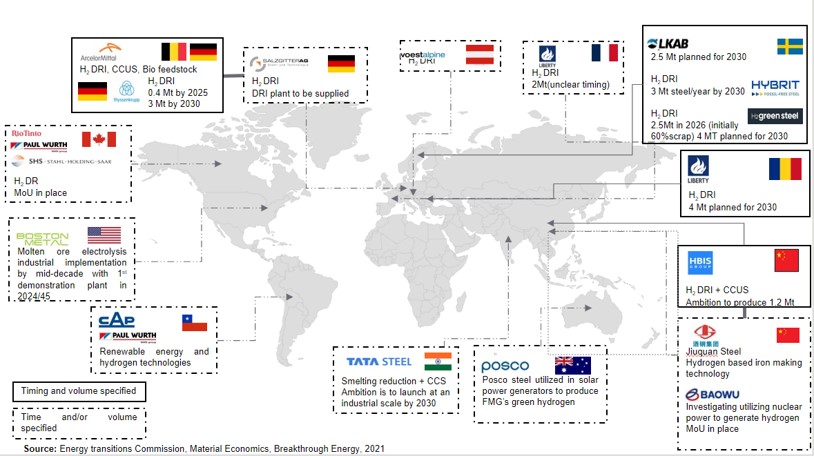

Key initiatives taken by steel producers for decarbonization

The hard-to-abate steel industry has rapidly embraced low CO2 production technologies in the recent 3-4 years, evident in the surge of planned investments. As of the end of 2021, over 90% of global steelmaking and crude steel production companies were in countries with announced net-zero targets, with 30% of steel companies covered by corporate net-zero targets. Major players in this regard are ArcelorMittal, ThyssenKrupp, SSAB/LKAB/Vattenfall, Nippon Steel and POSCO. European companies typically lead the pack in setting net-zero targets, followed by the Asian and Chinese ones (Exhibit 5). SSAB, a Swedish steel company, aims to deliver fossil-free steel at a commercial scale from 2026 and has already produced the first steel made of hydrogen-reduced iron in 2021. SSAB’s partnerships with Epiroc and involvement in the HYBRIT initiative, alongside LKAB and Vattenfall, demonstrate efforts to eliminate carbon dioxide emissions in steel production. Similarly, ArcelorMittal is planning to reach a net-zero emissions target by 2050 by investing in hydrogen-ready DRI technology. The company has plans to install H2-ready DRI-EAF technologies in Canada and other developed countries such as Spain, France, Belgium and Germany. The AI Reyadah project in Abu Dhabi, UAE, is the sole commercial scale project of CCS applied to an existing steel plant. The captured CO2 is injected into the oil field for enhanced oil recovery.

Though green steel lacks a defined standard presently, the interest in green steel certification has surged in recent years. Existing green standards focus on emissions or production processes, with qualifying thresholds for emissions intensity ranging from 2.5 tonnes of CO2 to nearly zero per tonne of crude steel. For informed decision-making and transparency, it’s crucial for governments and industry alliances to collaborate on defining and aligning standards, certifications and narrowing the tolerance bands over time to ensure credible actions.

What is in it for the end consumer?

Steel contributes to approximately one-third of supply chain and manufacturing emissions for buildings and cars, and close to half in white goods and renewable energy equipment. Serving as the starting point for many supply chains, steel’s impact is substantial.

At FutureBridge, we emphasize that steel decarbonization is a global challenge requiring collaboration across the industry supply chain. Accelerating the transition to a 1.5°C pathway demands coordinated market, regulatory, and financial interventions. This can be achieved through:

- Stimulating Demand: Governments can stimulate demand for green steel by implementing mandates for low-carbon steel procurement policies. Introducing carbon taxes or equivalent mechanisms can help reduce the cost advantage of high-carbon manufacturing, supporting the higher costs of transition.

- Technology Selection: Businesses, considering the nature of their industrial facilities, should select appropriate technology and procurement pathways based on resource availability, geographical constraints, policy and regulatory support, and associated cost implications.

- Partnerships and Collaborations: Businesses, recognizing the shared interest in decarbonizing industrial processes, should establish partnerships to collaborate and scale up innovative technologies.

Above all, raising public awareness about the benefits of green steel is vital for driving demand through encouraging adoption across all steel-consuming industries.

For tailored strategies in steel decarbonization, collaborate with FutureBridge experts. We emphasize global collaboration for a sustainable 1.5°C pathway.