Article

In-vehicle Payment Systems – Connected Commerce is the Next Consumer Choice

Mobility

Introduction

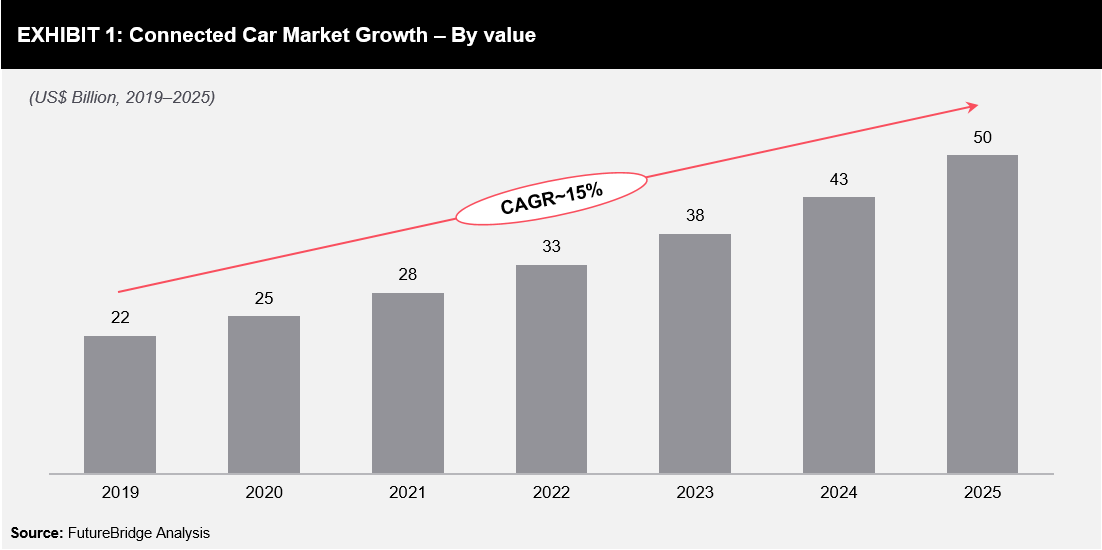

In-car payment systems are one of the most prominent Human-Machine-Interface trends in the mobility industry with rapid growth in autonomous and connected vehicles (refer to Exhibit 1). In addition, 5G and improved Wi-Fi connectivity are also expected to increase the adoption of in-car payment systems. Payment functionality in vehicles are enabled through:- RFID tags that can send payment data over-the-air

- Embedded BLE hardware modules that can transmit data at a higher range

Key Initiatives for In-vehicle Payment Solutions

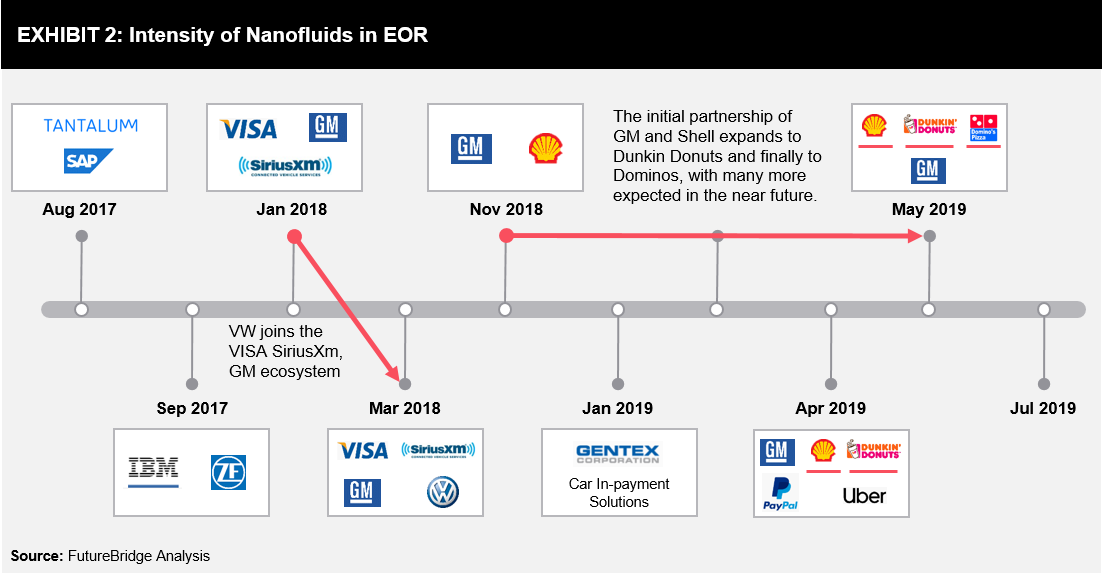

The concept of in-car payment systems is not very new; however, there has been an increased penetration since 2017 (refer to Exhibit 2). Companies such as General Motors, Volkswagen, and ZF Friedrichshafen have undertaken initiatives towards customer excellence and partnered with entities in the value chain to offer seamless in-car payment solutions experience.

Some other latest (in 2019) prominent initiatives are listed as follows:

In 2019, Hyundai partnered with Xevo (a leader in connected-car and automotive telematics technologies) for telematics solutions in the US and Europe.- The platform will provide Hyundai vehicles with access to engage and interact with favorite merchant brands and services through an easy-to-use interface on the in-vehicle touchscreen and mobile app.

- The offerings will include fuel, parking, and dining, as well as the digital payment feature.

- Merchants can promote their featured products by prompting touchscreen notifications on the driver’s screen.

- The platform combines cloud and edge services with a partner network that helps companies accelerate their development of connected vehicle solutions.

- In this partnership, along with other services such as OTA and telematics, Telenav is working on connected cloud and in-vehicle services for automotive infotainment, in-car commerce, and navigation.

- Customers can order food, save money on fuel purchases, and make dinner reservations via a touchscreen.

- It also allows drivers to locate and pay for nearby parking and schedule service appointments at FCA US dealerships.

- Smart Wallet will alert drivers on traffic conditions and offer alternate routes, thereby reducing fuel consumption and vehicle emissions.

- Users sharing this data will be rewarded with credits, which could be redeemed for rewards, paying tolls, and parking fees or for charging electric vehicles.

- Technology is being tested at their facility in Shannon, Ireland, where several cars, including the F-Pace and the Velar, are equipped with Smart Wallet.

Ecosystem of Payment System Providers

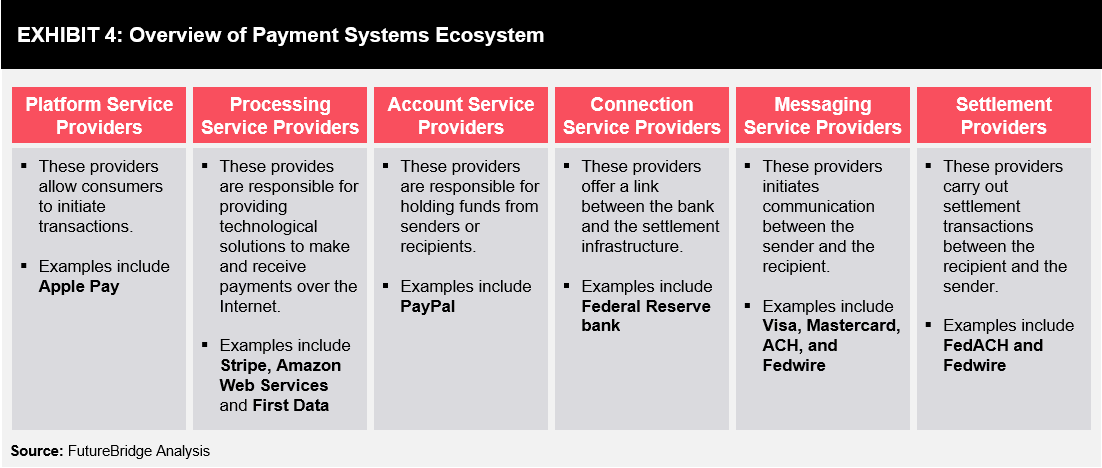

Key participants in the payment systems ecosystem include platform, processing, account, connection, messaging, and settlement providers (refer to Exhibit 4). These participants abide by the regulations and guidelines prevalent in their respective geographies and are responsible for handling transactions till settlement. Mostly, banks govern payment systems within individual countries. However, with the introduction of the revised Payment Services Directive (PSD2) by 2020 in the EU, there will be changes in the ecosystem with more competition, innovation, and transparency within the payments sector.

PSD2 ensures increasing customer protection and competition; this directive enables bank customers to use third-party providers (fintech companies) for managing their finances. Banks can no longer hold customer account information and will have to share it with third-party providers, thereby opening the doors for third-party providers to innovate their financial services. Banks will face stiff competition from third-party providers.

In addition, the new regulation opens up two key approaches:

Mostly, banks govern payment systems within individual countries. However, with the introduction of the revised Payment Services Directive (PSD2) by 2020 in the EU, there will be changes in the ecosystem with more competition, innovation, and transparency within the payments sector.

PSD2 ensures increasing customer protection and competition; this directive enables bank customers to use third-party providers (fintech companies) for managing their finances. Banks can no longer hold customer account information and will have to share it with third-party providers, thereby opening the doors for third-party providers to innovate their financial services. Banks will face stiff competition from third-party providers.

In addition, the new regulation opens up two key approaches:

- Payment initiation through Payment Initiation Providers who can initiate payments on behalf of the user

- Account Information Service Providers, who have access to the account information of bank customers

- These providers can have consolidated information of a single user from multiple bank accounts and will be able to analyze customer spending behavior.

Future Ahead

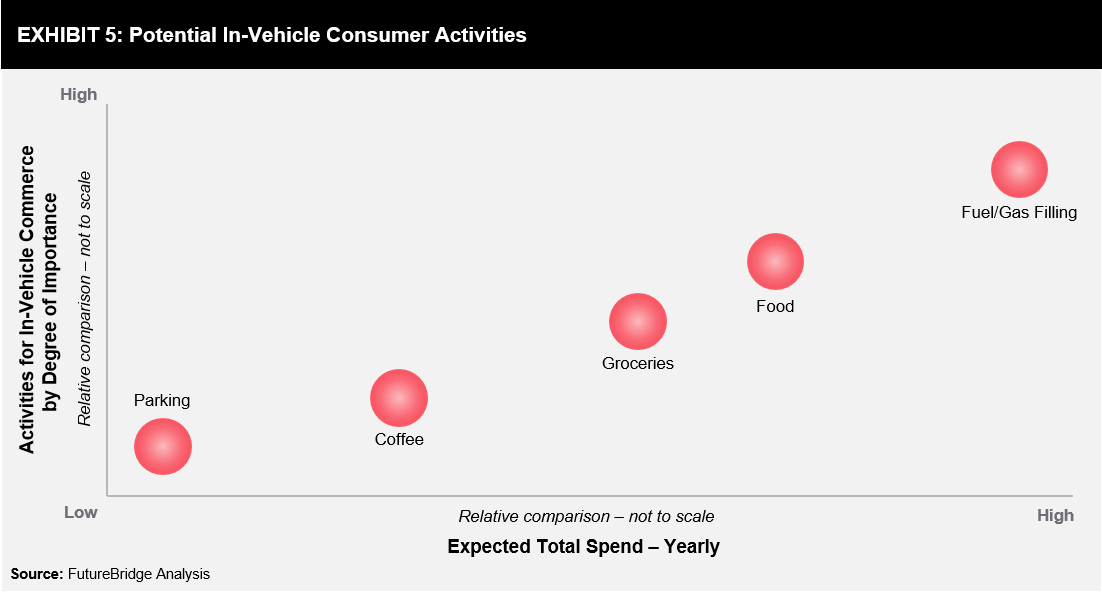

The market for in-car payment solutions is expected to increase significantly worldwide with a rise in the number of connected cars. Various players in the traditional ecosystem are identifying different avenues that could help enhance their market share either through revenue generation, product expansion, or customer loyalty. According to estimates, the in-vehicle commerce market holds >USD200 billion market opportunity, which is expected to grow significantly in the next 3–5 years. Some of the key activities (refer to Exhibit 5) among consumers include ordering coffee, searching for parking lots, ordering food & grocery, and searching for a gas station. Fuel/gas filling is expected to be the highest spend and most popular in-vehicle commerce activity among commuters, globally. Due to this, significant opportunities are expected across the value chain:

Due to this, significant opportunities are expected across the value chain:

- Payment Service Providers: Payment service providers will have ample opportunities for creating alliances between them and stores, gas stations, etc.

- They will act as an intermediary between retailers, consumers, and fleet operators. This will provide payment service providers with opportunities to create customer-oriented tools. They can act as a helping intermediary for OEMs, advising them on critical aspects of payment features available in the existing vehicles as well as future vehicles.

- They will also have opportunities to consolidate ample data available across multiple systems and functions. This data will be analyzed, which, in turn, will help create and maintain standards, such as authentication, risk modeling, and tokenization.

- OEMs: OEMs will have the opportunity to innovate future vehicles with additional features and attract customers by offering a seamless driving experience.