Blog

IVL Acquires Huntsman’s Chemical Intermediate and Surfactants Business

Energy

Indorama closes the largest-ever deal with Huntsman, valued at $2.1 billion

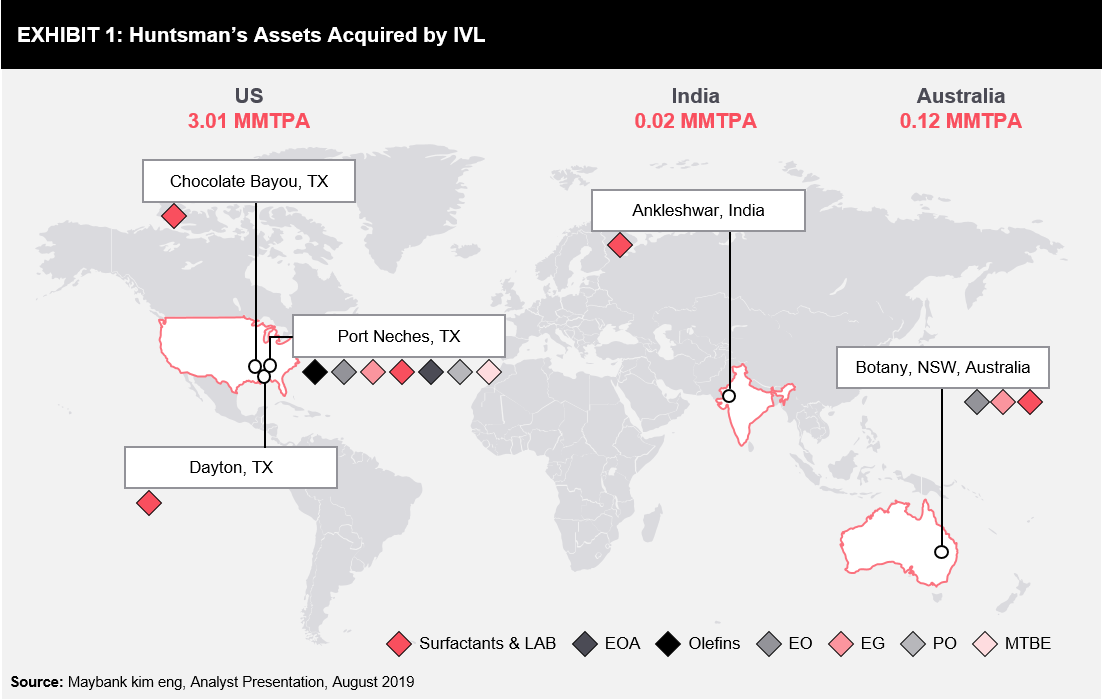

On January 6, 2020, Thailand-based Indorama Ventures Public Company Limited (IVL) completed its largest-ever deal by acquiring Texas-based Huntsman’s (HUN) chemical intermediate and surfactants business. The deal valued $2.0 billion in cash and up to $76 million in pension obligations. IVL expects to fund the deal with short-term loans of ~$1.5 billion, and the rest from its operating cash flows. According to IVL’s official website, this deal corresponds to an EV/EBITDA multiple of 5.7 and aligns well with the company’s stated goal of doubling its core EBITDA by 2023. For Huntsman, it is a part of its diversification strategy, allowing it to focus on its growing Polyurethanes and Advanced Materials businesses. The divesture also marks Huntsman’s complete exit from the US ethylene business, which the company had built following a series of acquisitions, the largest one being ICI’s base chemicals business. The terms of the agreement include the acquisition of Huntsman’s manufacturing facilities in three countries, with five production facilities – located at Port Neches, Texas; Dayton, Texas; Chocolate Bayou, Texas; Ankleshwar, India; and Botany, Australia. The combined assets of Huntsman include production assets worth 3.1 million tons, with >95% of production capacity located in Texas. Along with a strong asset portfolio, the acquisition also combines a strong management and workforce team of ~1200 Huntsman employees and a transfer of ~900 patents as well as other intellectual properties. The production assets at Port Neches, Texas, include a ~236 KTPA mixed-feed cracker, a 1 million tons/year Ethylene Oxide (EO)/Monoethylene Glycol (MEG) unit, and a propylene oxide/Methyl Tertiary Butyl Ether (MTBE) plant that produces surfactants and amines. The Chocolate Bayou facility in Houston, and Dayton, Texas, produce Linear Alkyl-Benzene (LAB) and surfactants, respectively. IVL has historically been strong in the PET business, while this acquisition further establishes its credibility in the US market by strengthening the PET feedstock supply chain (ethylene/EO/MEG). It also adds some new downstream products to IVL’s portfolio, such as propylene/propylene oxide derivatives, surfactants, ethanolamines, glycol ethers, and MTBE. Most of these products serve niche markets and industries addressing customer needs on a daily basis, growing at an average rate of >5% per annum.

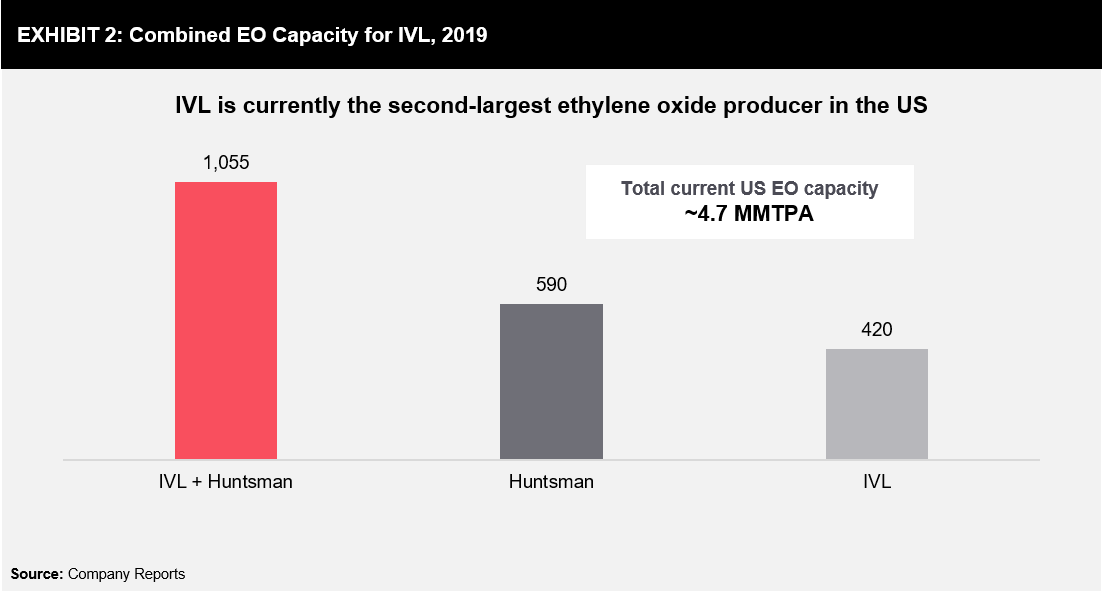

This acquisition adds another feather in IVL’s portfolio, making it the second-largest EO producer in the US. As a part of its strategy to achieve end-to-end integration in the ethylene value chain, earlier in 2019, the company restarted its Lake Charles, Texas, steam cracker to provide full backward integration. The refurbished gas cracker capacity presently stands at 440 KTPA, an increase of ~70 KTPA from its 2015 capacity levels; the plant will resume operations in Q1, 2020. The company also has a 550 KTPA MEG plant in Texas, US.

The production assets at Port Neches, Texas, include a ~236 KTPA mixed-feed cracker, a 1 million tons/year Ethylene Oxide (EO)/Monoethylene Glycol (MEG) unit, and a propylene oxide/Methyl Tertiary Butyl Ether (MTBE) plant that produces surfactants and amines. The Chocolate Bayou facility in Houston, and Dayton, Texas, produce Linear Alkyl-Benzene (LAB) and surfactants, respectively. IVL has historically been strong in the PET business, while this acquisition further establishes its credibility in the US market by strengthening the PET feedstock supply chain (ethylene/EO/MEG). It also adds some new downstream products to IVL’s portfolio, such as propylene/propylene oxide derivatives, surfactants, ethanolamines, glycol ethers, and MTBE. Most of these products serve niche markets and industries addressing customer needs on a daily basis, growing at an average rate of >5% per annum.

This acquisition adds another feather in IVL’s portfolio, making it the second-largest EO producer in the US. As a part of its strategy to achieve end-to-end integration in the ethylene value chain, earlier in 2019, the company restarted its Lake Charles, Texas, steam cracker to provide full backward integration. The refurbished gas cracker capacity presently stands at 440 KTPA, an increase of ~70 KTPA from its 2015 capacity levels; the plant will resume operations in Q1, 2020. The company also has a 550 KTPA MEG plant in Texas, US. EO derivative products are expected to grow in the range of 5-6% per annum till 2023. Likewise, the new portfolio entrant for IVL, the PO derivatives are expected to grow in the range of 4-5%. The interesting aspect to observe is how IVL nurtures Huntsman’s legacy of being one of the lowest cash cost producers of PO. In addition, MTBE, used as a gasoline blendstock to reduce emissions, will be imported to nearby markets, such as Latin America, due to a ban in the US market. However, its demand is expected to grow in the range of 3-4% per annum.

EO derivative products are expected to grow in the range of 5-6% per annum till 2023. Likewise, the new portfolio entrant for IVL, the PO derivatives are expected to grow in the range of 4-5%. The interesting aspect to observe is how IVL nurtures Huntsman’s legacy of being one of the lowest cash cost producers of PO. In addition, MTBE, used as a gasoline blendstock to reduce emissions, will be imported to nearby markets, such as Latin America, due to a ban in the US market. However, its demand is expected to grow in the range of 3-4% per annum.

Synergies from the acquisition

Last year, IVL, in its earnings presentation, clearly stated its aspirations of being a strong player in the ethylene derivatives and specialty chemicals business. This acquisition reinstates the company’s desire to gain direct entry into several end-application industries growing at a rapid pace; these industries include home & personal care; consumer goods, such as detergents, cleansers, shampoo, and furniture; automotive parts; and fuels and lubricants. Talking of the deal in terms of expected synergies that it brings for IVL’s business, the company claims to achieve benefits of $100 million by FY2023. This is primarily attributed to three factors:- Cost reduction synergies from similar businesses

- Gaining a strong foothold in the new downstream business and special products with high margins

- Achieving operational excellence by improving certain production processes