How do EVs contribute to Grid Flexibility?

Grid flexibility is the answer to rising load demand and variability

Power utilities across the US, Europe, and Asia are operating grids built for a different era, with predictable demand and stable generation. Those conditions no longer hold.

Electricity demand is set to roughly double by 2050, with Europe alone expected to add around 460 TWh by 2030, driven by EVs, data centers, and industrial electrification. Similar trajectories are visible across North America and Asia.

At the same time, wind and solar capacity is expected to grow nearly ninefold globally. This is increasing variability and curtailment, which could reach 100 to 310 TWh annually in Europe by 2040 if the grid is not adapted.

The structural reality: rising demand and rising variability are converging faster than grid upgrades can keep pace. Traditional reinforcement cycles cannot carry the full burden.

Grid flexibility offers a practical solution.

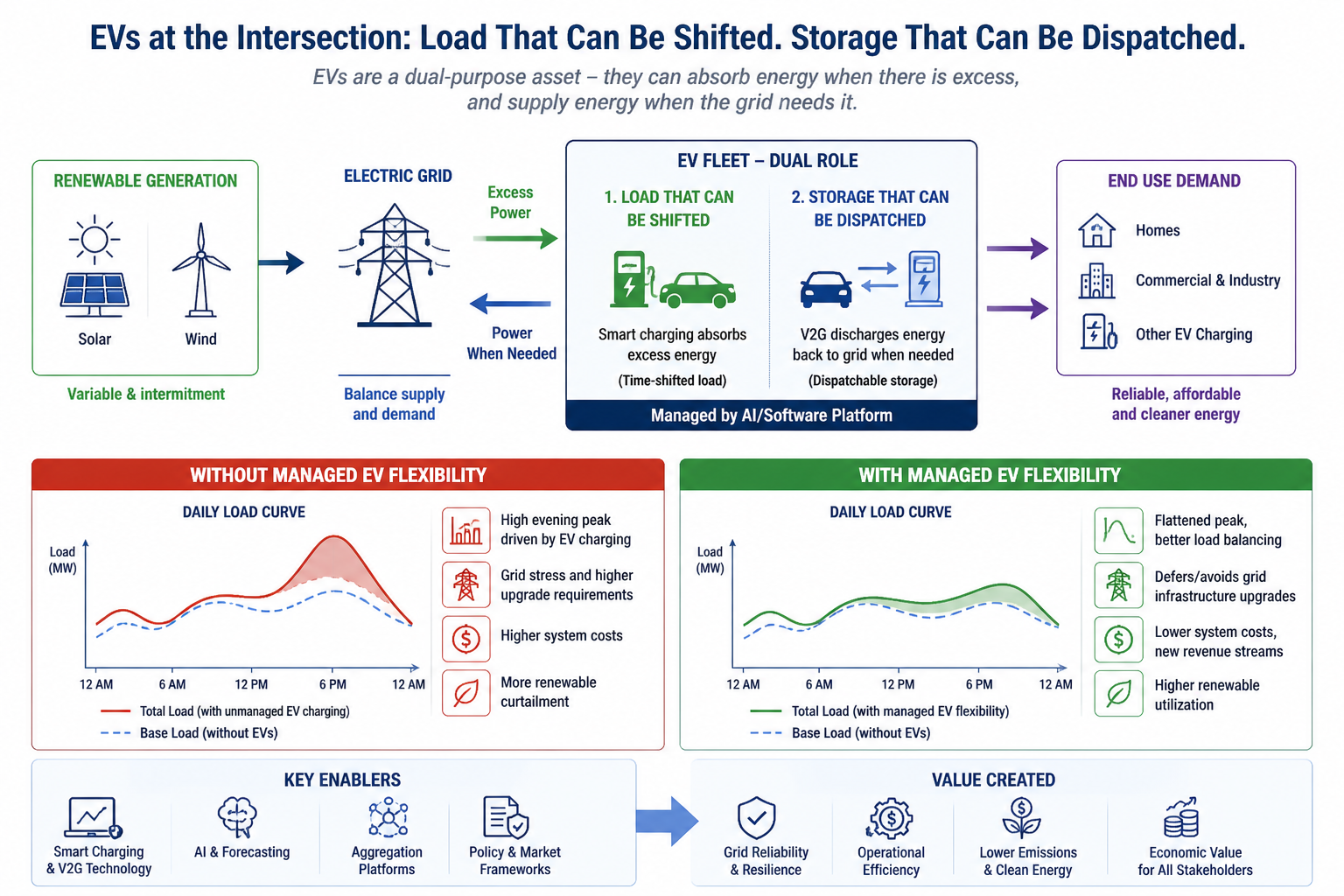

Managed at scale, EVs act as flexible load and distributed storage, helping balance both sides of the equation in real time.

For a detailed view of how this distinction flows through to power-utility margins, explore the full grid resiliency vs reliability analysis

Power utilities across the US, Europe, and Asia are managing infrastructure designed for a different era: predictable demand curves, dispatchable inertia-rich generation, and long asset replacement cycles. None of those assumptions hold the way they used to.

Global electricity demand is on track to double by 2050 from 2020 levels. Europe alone will absorb roughly 460 TWh of additional demand by 2030, driven by EV adoption, data centers, industrial electrification, and hydrogen production. North America is following a similar trajectory. In Asia, the pace is faster as China, India, and South Korea manage rapid electrification against grids that were not originally designed for it.

In parallel, wind and solar capacity is expected to grow nearly ninefold globally by 2050. Renewable curtailment in Europe alone is projected to reach 100 to 310 TWh annually by 2040 under business-as-usual grid conditions, while parts of Asia are already treating curtailment as a recurring operational cost today.

EVs sit at the intersection. Managed at scale, they are load that can be shifted and storage that can be dispatched.

This dual role makes EV flexibility a direct, near-term lever for handling both demand growth and renewable variability without waiting for long-cycle grid reinforcement.

The cost of grid inflexibility is compounding

EU congestion management costs exceeded 4 billion euros in 2023, with Germany alone accounting for around 60% of that spend. This excludes imbalance penalties, peak reserve capacity, and revenue losses from curtailed renewables.

In the US, FERC Order 2222 reflects the growing cost of not dispatching distributed resources. In Japan and South Korea, utilities are still managing frequency stability with limited flexible assets, absorbing higher operating costs and risk.

Direct P&L impact

- Higher congestion and redispatch costs

- Elevated balancing and reserve requirements

- Lost revenue from curtailment and constrained assets

Strategic risk

- Inability to absorb new electrification load

- Delayed connection of new renewables and flexibility assets

- Margin erosion as variable costs outpace revenue growth

These costs are already visible in earnings. They are persistent, and they increase as renewable penetration rises if flexibility is not integrated into the operating model.

Smart charging (V1G): Incorporating immediate grid flexibility without complexity

Unidirectional smart charging delivers immediate grid flexibility without new hardware, market redesign, or major regulatory change. It simply controls when EVs charge. Drivers set preferences, and charging shifts to lower-cost periods, relieving peak load when grid stress is highest.

System-level value

Studies indicate up to 4 billion euros in estimated annual savings for European grid operators from optimized flexibility, with smart charging as a key driver.

Market evidence

Market data from PJM, CAISO, and ERCOT shows lower balancing costs as flexible load grows, while deployments in China have already reduced peak transformer loading in major cities.

The challenge is not technology. It is participation and integration: scaling time-of-use pricing, aligning incentives, and ensuring data interoperability across diverse vehicle fleets and systems.

Vehicle-to-Grid (V2G): Unlocking distributed storage at scale

V2G enables bidirectional power flow, allowing EVs to supply energy back to the grid or buildings. This turns EVs from passive loads into dispatchable storage assets.

Potential EV battery capacity in Europe by 2030 under flexibility scenarios

Potential reduction in global peak demand by 2035 from smart charging and V2G

The advantage is location: EV batteries are distributed across the same urban and peri-urban areas where grid congestion is highest, providing storage without the delay and cost of large central infrastructure.

Barriers remain, including low penetration of bidirectional chargers, limited standardisation, and evolving battery warranty frameworks. These are transitional challenges. The technologies are proven, and regulatory and market designs are catching up.

Global V2G adoption is outpacing power utility readiness

Global V2G adoption is advancing at different speeds, with clear strategic implications. Power utilities focused only on their local markets risk underestimating how quickly commercial frameworks are maturing elsewhere.

Europe

EVs represented about 22–23% of new vehicle sales in 2024, with a confirmed 2035 phase-out of internal combustion. V2G regulations on data, metering, and market access are among the most advanced globally.

United States

Policy support and FERC Order 2222 are enabling aggregation of distributed resources, while utilities are piloting V2G across school buses, fleets, and residential programs.

Asia

China, Japan, and South Korea are scaling EV adoption rapidly and advancing grid integration standards, with V2G already being trialed in key metropolitan areas.

The direction is clear: V2G will scale. The real question is whether utilities will be operationally and commercially ready when their markets reach that inflection point.

How V2G economics is reshaping grid investment decisions

Three numbers define the emerging V2G business case:

Invested in flywheel-based inertia

Offshore wind integration supported

Instantaneous renewable operation enabled

How Grid Flexibility Investments Delivered Outsized Returns

A leading example from Ireland demonstrates the economic impact of targeted investment in grid flexibility.

Strengthen grid stability, enable higher renewable penetration, and avoid major infrastructure spend through targeted flexibility investment.

Invested in flywheel-based inertia

Offshore wind integration supported

Instantaneous renewable operation enabled

System Impact

- Retirement of a coal plant

- Supported integration of 1,500 MW offshore wind

- Allowed up to 100 percent instantaneous renewable operation

Avoided Infrastructure Requirements

- Fossil backup capacity

- Large-scale transmission upgrades