Beyond Compliance: The Strategic Shift to Fluorine-Free Switchgear

The Shift Away From SF₆ Is No Longer About Sustainability Alone

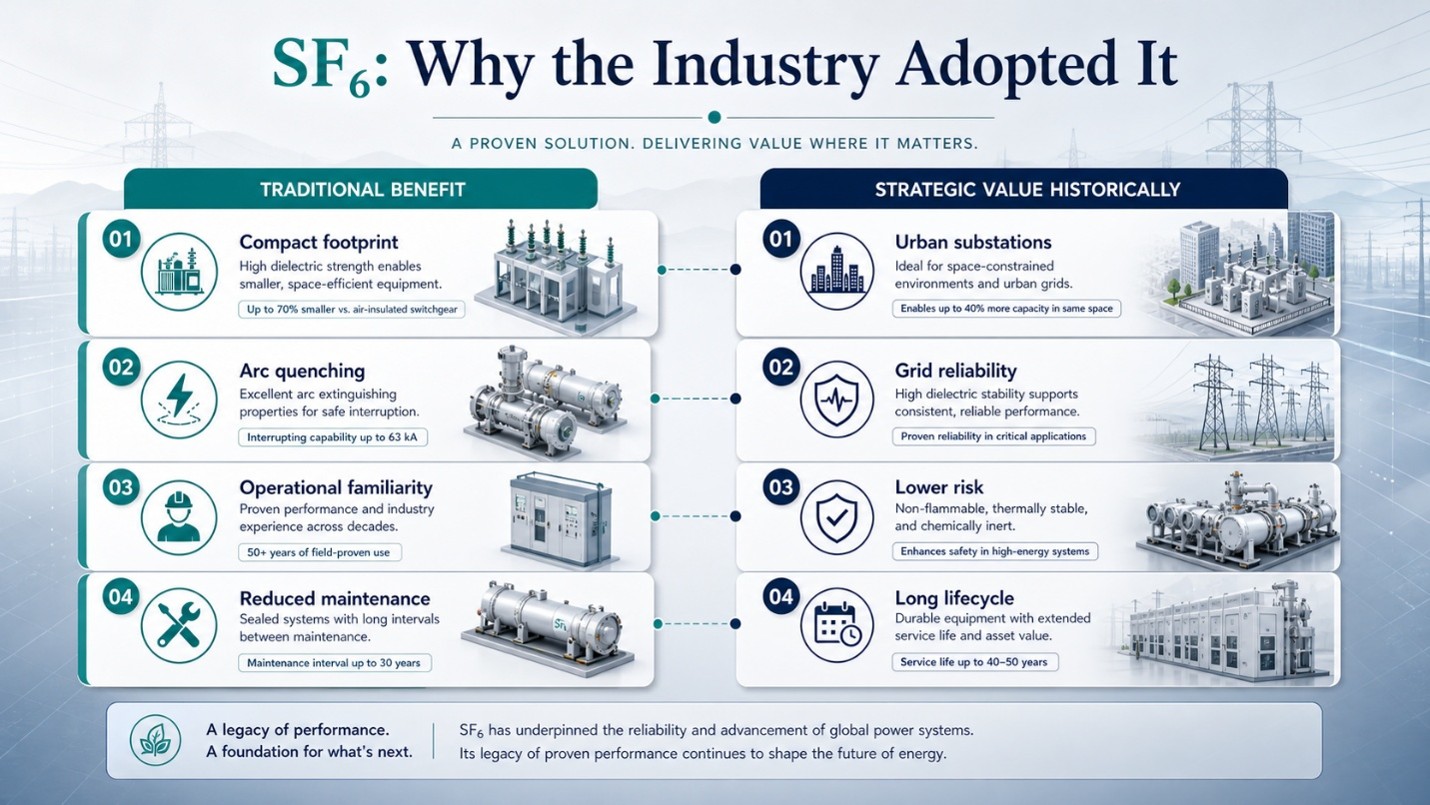

For more than 50 years, sulfur hexafluoride (SF₆) has been the insulation gas of choice in switchgear due to its reliability, stability, and compact design. But the conversation around SF₆ is changing. While its environmental impact has long been a concern, regulatory pressure is now turning that concern into action. SF₆ has a global warming potential approximately 23,500 times higher than CO₂ and can remain in the atmosphere for over 3,000 years. With phase-out regulations now taking effect including the first medium-voltage (MV) restrictions the transition away from SF₆ has become a compliance and business imperative, not just a sustainability goal. It allowed utilities to build compact substations beneath cities, stabilize industrial power systems, and expand transmission capacity where space constraints made conventional systems impractical. Very few technologies became as deeply embedded into medium and high-voltage infrastructure planning.

Very few people outside the switchgear industry paid attention to SF₆. Now utilities, regulators, investors, infrastructure lenders, and OEM boardrooms are all paying attention.

What changed is not simply environmental awareness. What changed is that long-life infrastructure assets are suddenly colliding with rapidly evolving regulatory systems, financing standards, and procurement expectations. Grid infrastructure designed for forty-year operating cycles is now being evaluated against policy horizons that shift every four to five years.

This transition is no longer only about emissions reduction. It is now about whether assets can stay compliant, bankable, easy to operate, and resilient over decades.

In 2026, utilities are not comparing SF₆ and fluorine-free switchgear on insulation performance alone. They are weighing two very different infrastructure paths: one exposed to tightening regulation, rising lifecycle risk, and potential financing constraints; the other better aligned with long-term grid investment, simpler compliance, and resilient network planning.

SF₆ was never a technological mistake

The easiest way to misunderstand the current transition is to assume the industry irresponsibly ignored sustainability concerns for decades.

It did not.

Utilities adopted SF₆ because the technology solved extremely difficult engineering problems exceptionally well. SF₆ offered high dielectric strength, reliable arc quenching, smaller equipment footprints, lower maintenance complexity, and operational familiarity utilities trusted deeply. In dense urban substations, offshore infrastructure, and industrial facilities, SF₆-enabled GIS often made electrification economically viable in the first place.

Historically, utilities are optimized around three core variables

- Reliability

- Cost efficiency

- Space optimization

Today, a fourth variable has become unavoidable: Regulatory permanence. That single shift is fundamentally changing procurement behavior across utilities, infrastructure investors, and OEM ecosystems.

The regulatory push to meet climate compliance: exact deadlines and obligations

Regulation (EU) 2024/573 — the binding F-Gas Regulation

Adopted March 2024 and effective from the same date, this regulation replaces the 2014 F-Gas Regulation (517/2014) and sets legally binding phase-out dates for SF₆ and all F-gases in new electrical switchgear placed on the EU market.

| Effective Date | Scope / Equipment Covered | Requirement / Restriction |

|---|---|---|

| 1 Jan 2026 | Medium-voltage (MV) switchgear ≤ 24 kV | Full ban on new SF₆-based switchgear (distribution GIS and RMUs) |

| 1 Jan 2028 | 52–145 kV high-voltage (HV) switchgear (≤50 kA short-circuit current) | Ban on all new F-gas (GWP ≥1) switchgear |

| 1 Jan 2030 | Medium-voltage (MV) switchgear 24–52 kV | Full ban on new F-gas switchgear |

| 1 Jan 2032 | Extra-high voltage (EHV) switchgear >145 kV (including HVDC converter stations) | Ban on all new F-gas switchgear |

| 1 Jan 2035 | All existing switchgear (any voltage level) | Prohibition on use of newly produced SF₆ for servicing/maintenance; only reclaimed/recycled SF₆ allowed where no alternative exists |

EU Regulation 2024/573 bans SF₆ and fluorinated gases in new switchgear:

- Eco-mix alternatives like fluoroketone (C5FK) and fluoronitrile (C4FN) count as F-gases.

- Only air (N₂/O₂) with vacuum interruption ensures full compliance.

- Similar rules are advancing in California (CARB 2025), New York, UK, and China.

The Business Imperative: why this has moved to the boardroom

Four drivers have taken this beyond engineering departments:

- Total cost of ownership. SF₆ systems carry unavoidable OPEX that most operators have absorbed without scrutiny, including gas leak checks every six years, certified technician recertification every seven, gas inventory reporting, and end-of-life recovery. None of this creates value. Fluorine-free eliminates the entire governance structure. Documented lifecycle cost savings: 20–30%.

- Compactness no longer requires SF₆. The reason SF₆ dominated was its ability to deliver compact GIS where AIS cannot fit urban basements, kiosks, or offshore platforms. Fluorine-free GIS now delivers the same footprint, up to 60% smaller than AIS. The space constraint remains; the dependency on SF₆ to solve it does not.

- F-gas governance is a growing operational burden. EU obligations for SF₆ equipment are active and intensifying leak repair, threshold-triggered checks, certified recovery personnel, gas inventory records. Fluorine-free removes the operator from this compliance cycle entirely, eliminating specialized handling equipment and mandatory gas quantity reporting.

- ESG and financing covenants. Infrastructure funds and project lenders are embedding no-SF₆ requirements in loan agreements. North Sea and Baltic offshore wind financing routinely specifies fluorine-free equipment. Equipment choice has become a financing decision made at project inception.

- Stranded asset risk. MV switchgear lasts 35–40 years. SF₆ equipment commissioned today will be in service past 2060, through the 2035 virgin-gas servicing restriction and every subsequent tightening. Compliance liability does not depreciate with the asset. It compounds.

The Engineering Challenge by Voltage Band

6–24 kV: Immediate deadline, mature technology

Covering secondary distribution, urban RMUs, data centers, and industrial facilities — the largest volume segment, facing the earliest deadline. The technology is ready:

- Same footprint, no civil rework. ABB UniSec Air is designed with identical footprint, operations, and backward compatibility to its SF₆ predecessor – panel-for-panel brownfield replacement without room modifications.

- Arc safety proven. Clean Air produces no toxic decomposition byproducts during switching, a material safety improvement in occupied indoor environments.

- Long service life. Hermetically sealed, welded stainless steel vessels provide environmental independence from humidity, dust, and wildlife. Stated service life: ≥35–40 years across leading platforms.

24–52 kV: 2030 deadline, solvable with discipline

Covering renewable collectors, offshore platforms, and primary distribution. More demanding engineering, but solutions exist:

- Insulation gap is bridged through optimized field control, solid insulation interfaces, and sealed vessel design – compensating for clean air’s lower dielectric strength vs. SF₆.

- Harsh environment resilience. Hermetically sealed vessels eliminate ingress from coastal salt air, desert dust, and wildlife, reducing failure accelerators in open equipment at remote sites.

- High switching endurance. Vacuum interruption separates arc-extinction from insulation, handling multi-feeder collector switching duty without degrading dielectric performance.

- Avoid the eco-mix trap. Fluoroketone and fluoronitrile remain regulated F-gases. Specifying fluorine-free now removes mid-life requalification risk as regulation tightens.

Real-World Deployments

Siemens / EWD — 8DAB 24 Blue GIS, Davos, Switzerland (24 kV)

Siemens installed and commissioned the world’s first 8DAB 24 blue GIS medium-voltage system at the Dorf substation in Davos, Europe’s highest city at 1,560 meters above sea level. This is a landmark deployment: a Clean Air GIS validated in an extreme alpine environment with harsh winter conditions, temperature cycling, and high altitude, directly answering questions about fluorine-free performance outside controlled settings. Driver: EWD’s commitment to climate-neutral power distribution, with the utility stating that a like-for-like alternative without the environmental disadvantage of SF₆ warranted an immediate switch.

E.ON / ABB: SafeRing & SafePlus Air, Germany (24 kV)

E.ON (800,000+ km grids, 60% of Germany’s customers) selected ABB’s 24 kV GIS for network-wide rollout before 2026. Drivers: early compliance, emissions cuts, and seamless swap with identical footprint and procedures as SF₆ units.

What This Means for OEMs?

The picture is more nuanced than a simple “SF₆ is dead” narrative. The transition is real but uneven across markets, and OEMs that misread the geography will make poor portfolio decisions in either direction.

- In Europe, SF₆ is effectively a sunset technology for new MV equipment. The 2026 and 2030 deadlines are not negotiable. OEMs that do not have a qualified, production-ready fluorine-free ≤24 kV platform are already being excluded from EU tenders. Framework agreements are locked with manufacturers that have reference installations. This is not a future risk — it is the current commercial reality in the EU market.

- Outside Europe, the picture is different, and OEMs need both portfolios. India is expanding its grid at a pace that few other markets match; it is adding transmission and distribution infrastructure at scale, and SF₆-based switchgear remains entirely legal, commercially competitive, and actively procured there. The same applies across Southeast Asia, the Middle East, and large parts of Africa. The US is a split market: California and New York are restricting SF₆, but federal procurement and most state-level utilities continue to specify it. An OEM that abandons SF₆ prematurely to chase EU compliance will forfeit commercially significant volume in growth markets.

- The eco-mix position requires careful re-evaluation. OEMs selling fluoroketone or fluoronitrile blends as “SF₆-free” now face a sharper challenge in Europe: customers are asking whether the solution is truly F-gas-free, not just SF₆-free. Outside EU-regulated markets, these eco-mix products still have a role. They lower emissions versus SF₆ and can be a practical bridge. But in Europe, the buying logic is shifting toward clean air, vacuum, and other fluorine-free options that remove future compliance risk.

What This Means for TSOs and DSOs?

For transmission and distribution operators, the challenge is not just procuring the right equipment. It is managing a transition across large, heterogeneous networks where standardization is incomplete; field experience is limited, and the consequences of getting it wrong are measured in decades.

- Standardization is genuinely incomplete, and that creates procurement risk. IEC, CIGRE, and IEEE are actively updating frameworks for SF₆-free alternatives, but the process takes a decade by design. One of the industry’s current challenges is that standards for fluorine-free medium-voltage switchgears are still evolving. Testing methods, maintenance practices, gas-handling requirements, and interoperability guidelines are not yet fully harmonized across voltage classes or regions. As a result, utilities specifying fluorine-free equipment today are often moving ahead of the standards curve, relying more heavily on OEM data, field experience, and project-specific validation than on universally adopted industry frameworks.

- Brownfield replacement requires more planning than a product swap. The “same footprint” promise is real for many platforms, but it is not universal across all panel configurations, cable interface types, and room layouts. DSOs planning large brownfield programs should conduct a systematic bay-by-bay compatibility assessment before issuing tenders — identifying which installations can be swapped panel-for-panel and which require engineering work. Getting this wrong at the tender stage creates cost overruns and program delays that ultimately push delivery past the 2026 deadline.

Conclusion

Fluorine-free MV switchgear is no longer theoretical. Deployments from Paris to Davos to Milan confirm that it works in real operating environments.

The transition, however, remains uneven across regions, and clarity about where the market stands is now strategically important.

-

In Europe, the transition is no longer optional.

The 2026 deadline is live. Utilities still procuring SF₆ are not just accumulating regulatory risk; they are commissioning assets whose serviceability is set to deteriorate progressively through the 2030s. -

Outside Europe, SF₆ is not disappearing soon.

India, Southeast Asia, and the Middle East are expanding grids rapidly, and SF₆ remains legal, available, and cost-competitive. OEMs and utilities in these markets still have time to plan deliberately, but ESG financing covenants are beginning to extend beyond regulatory boundaries, and that window is narrowing. -

Two challenges will define the next decade:

-

Standardization.

IEC, CIGRE, and IEEE frameworks are still maturing. Operators specifying fluorine-free equipment today are doing so ahead of fully codified standards, and the long-term liability for a 40-year asset remains with the operator. -

Operational validation.

SF₆ has sixty years of field data across nearly every climate. Fluorine-free alternatives do not. First deployments should therefore be treated as instrumented learning assets, not merely compliance checkboxes.

-

Standardization.

-

The transition rewards early planners and rigorous specifiers.

The organizations that move early, validate thoroughly, and standardize intelligently will be best positioned as regulatory pressure, financing expectations, and procurement logic continue to converge.